An MSP's multiple climbs with three things: scale, recurring revenue mix, and focus. Everything else on the valuation checklist is a version of one of those. Cross an EBITDA threshold and buyers re-rate you into a higher band. Push recurring revenue past the line where the business reads as an annuity instead of a project shop, and the same EBITDA earns more turns. Own something scarce, a real cybersecurity capability or genuine vertical depth, and a strategic buyer will pay for it far above the market floor. That is the whole game in one sentence, and the rest of this piece is the detail underneath it.

I write this from the operator seat, not the broker seat. I spent a decade in investment banking and private equity working on over 7bn dollars of transactions, including a board seat through a 300m dollar-plus PE exit, and I now run growth inside a US MSP. So I see both halves: the finance math that sets the multiple, and the operating reality that either supports the number or quietly undermines it in diligence. The levers below are the ones that actually move the price in the deals I have watched, ranked by how much leverage an owner really has over them.

Every number here comes from our verified transaction work or from named, attributed sources. Where a figure is a practitioner's on-camera claim rather than confirmed deal data, I say so. For the underlying comp set and the full source reconciliation, start with the pillar: MSP valuation multiples in 2026.

How the levers stack

Before the individual levers, hold the ladder in your head. Multiples rise with company size in a fairly predictable way, and the levers below either push you up a rung early or hold you back a rung despite your size. Here is the published like-for-like size ladder our reconciliation lands on for US MSPs, expressed in EV/EBITDA.

| Size band | Working multiple range |

|---|---|

| Owner-run, sub-1M dollar EBITDA | 3 to 6x |

| 1 to 5M dollar EBITDA, lower-mid | 5 to 10x |

| Platform, 5M dollar-plus EBITDA | 10 to 15x |

The levers do not replace the ladder. They decide where inside a band you land, and, at the thresholds, whether you jump to the next one. A 900k dollar-EBITDA shop with 90 percent recurring revenue, clean contracts and a manager running delivery can price like the top of its band and read as a platform-in-waiting. A 900k dollar-EBITDA shop that is really the owner plus month-to-month clients prices at the floor, if it sells at all. Same EBITDA, different animal.

Here is the full set, with the direction each one pushes and the evidence behind it. Read the caveats in the sections that follow, not just the table, because the spikes are scarce cases, not the market you should plan around.

| Lever | Effect on multiple | Evidence |

|---|---|---|

| Recurring revenue mix | Raises turns as the business reads as an annuity, not a project shop | Advisors treat roughly 60 percent recurring as the line above which a business reads as attractive (Adam Borst, Vista Business Group) |

| Cyber / security scarcity | Large premium when the capability is genuinely scarce, not a bolt-on | Thales-Tesserent 24.1x and Datrix 16.3x as scarce-cyber strategic deals, against a break-fix floor of 2 to 7x (verified MSP comp set) |

| Size threshold | Re-rates you into a higher band at 1M and 5M dollar EBITDA | Platform status generally needs about 3M dollar-plus EBITDA before lenders engage (Abraham Garver, FOCUS Investment Banking); 5M dollar-plus EBITDA reaches the 10 to 15x band |

| Client concentration | Discounts the number, can force an earn-out structure | Lost recurring revenue between LOI and close triggered a 2M dollar valuation haircut in one advised deal (Abraham Garver) |

| Contract quality | Zero-contract clients fall to the break-fix bucket; multi-year paper supports higher turns | No-contract clients valued near a tenth of a contracted client's worth (Amy Babinchak, sell my MSP) |

| Owner dependence | Detachment lifts the multiple; a load-bearing owner drags it down | Quality-of-earnings review found 600k dollar EBITDA where the seller claimed 1M dollar, turning a 6M dollar deal into 3.6M dollar (Greg Bilzerian, NextGen Growth Partners) |

| Growth rate and pricing power | Buyers pay for forward growth; underpricing caps the ceiling | Growth trajectory weighted as a distinct lever from EBITDA size (Daniel Welling, MSP Finance Team) |

Recurring revenue mix

Recurring revenue is the first thing every buyer models because it is the thing they can underwrite. A managed-services contract that renews is an annuity a lender will lend against. A one-off migration project is a good quarter that may not repeat. When a buyer sees a book that is mostly recurring, the risk of the forecast drops, and lower risk is exactly what a higher multiple pays for.

The working line advisors use is roughly 60 percent recurring. Adam Borst of Vista Business Group calls that a pretty good number on air, the point above which a business reads as attractive and below which it gets less credit. He also warns against the opposite mistake, chasing 100 percent recurring by turning away easy project and product revenue that drops straight to cash. So the lever is not recurring at any cost. It is enough recurring that the base reads as durable, with project work layered on top rather than propping up the whole thing.

One caution that came up repeatedly in operator forums: contract paper without contract quality is a trap. A book full of month-to-month agreements counts as recurring on a spreadsheet but reads as churn risk to a buyer, which is why it lands closer to 4x than 5x in practitioner examples. Recurring revenue only helps the multiple when the revenue is genuinely sticky. For how buyers actually adjust for this in a full valuation, see how to value an MSP.

The cyber and security scarcity premium

This is the lever with the widest spread, and the one most likely to be misunderstood. Genuine, scarce cybersecurity capability can pull a deal far above the MSP size ladder. In our verified comp set, the strategic bucket's spikes were scarce capabilities: Thales acquiring Tesserent at 24.1x for sovereign cyber, and Datrix at 16.3x for cyber and cloud. Our region reconciliation flags the same pattern, and separate deals like ThirdSpace priced around 24.4x as a cyber add-on. Against those, the break-fix floor sits at 2 to 7x. That is a spread of more than 20 turns between a commodity shop and a scarce security capability.

| Deal or segment | EV/EBITDA | What it was |

|---|---|---|

| Thales-Tesserent | 24.1x | Sovereign cyber, strategic buyer paying for scarce capability |

| ThirdSpace | 24.4x | Cyber capability acquired as a strategic add-on |

| Datrix | 16.3x | Cyber and cloud capability |

| Break-fix / commodity MSP | 2 to 7x | The floor: undifferentiated managed IT |

Now the caveat, because it is the part vendors selling you a security bolt-on will not mention. These are scarce cases, not the market you should plan around. The premium is for a real, differentiated capability that a large acquirer finds cheaper to buy than to build. Abraham Garver of FOCUS Investment Banking is blunt about the softer version: cross-selling security to your existing base is now table stakes, not a premium driver. It is a one-time revenue bump, not a durable moat. Stapling a security line onto a break-fix shop does not move you toward 24x. It moves you toward the same 5 to 8x as everyone else, because every buyer can see it is a resold product, not a capability.

The scarcity that pays is the kind you cannot buy off a distributor: a genuine MSSP practice, a compliance niche a vertical actually needs, engineering depth a strategic cannot replicate quickly. If you have that, you are in the buyer-arbitrage story covered in who buys MSPs. If you have a resold security SKU, you have a cross-sell and the market multiple.

Size thresholds

Size is not a smooth slope. It steps. Two EBITDA thresholds re-rate you, and they matter more than any single turn of margin improvement because crossing one changes which buyers can even bid.

The first threshold is around 1M dollar EBITDA. Below it you are selling mostly to other owner-operators and search funds, the 3 to 5x world, often owner-to-owner sales that never reach a formal process. Reed Warren of iT Valuations, on the MSP Stack Podcast, puts roughly a quarter of the PE market as buyers only once a firm clears 1M dollar EBITDA, and about half the PE market active at 2M dollar-plus. Crossing 1M dollar opens the buyer pool, and a wider buyer pool is what actually bids the price up.

The second threshold is platform candidacy. Abraham Garver states plainly that platform status generally requires about 3M dollar-plus EBITDA, because below that the private credit lenders who fund a leveraged buyout will not engage, so smaller targets get folded in as add-ons rather than becoming platforms. Our own comp set makes the consequence concrete: PE platform and MBO deals priced at a 13.6x median, while PE add-ons, the tuck-ins, priced at 7.8x, the same as trade sales. The single most valuable re-rating in this market is going from tuck-in to platform, and the 5M dollar-plus EBITDA band, at 10 to 15x, is where that fully lands.

The honest read on buyer type, straight from our data, is this: it is not that PE pays more. Platforms get platform multiples. When PE buys you as the platform, you capture the re-rating. When a consolidator tucks you in, you get priced like a trade sale regardless of who ultimately owns the acquirer. Size is the lever that decides which side of that line you are on.

Client concentration and contract quality

Concentration is a discount waiting to happen. When one client is a large share of revenue, the buyer models the day that client leaves and prices the risk into the deal, or pushes the structure toward an earn-out so you carry the risk instead of them. Adam Borst notes that earn-outs, otherwise the exception in average MSP deals, show up specifically when there is high client concentration, one client above half of revenue, or when the business is very small. So concentration does not just cut the multiple. It changes how much of the money is guaranteed at close versus contingent on you hitting targets after you have lost control of the cost side.

Contract quality is the other half. The cleanest illustration of the downside came from Abraham Garver: in one advised deal, losing two or three clients worth about 200k dollars of recurring revenue between signing the LOI and closing triggered a 2M dollar valuation haircut at the buyer's insistence. Small concentration events get amplified into large price swings during diligence. On the paper itself, the operator view splits. Amy Babinchak of sell my MSP argues a long unwritten relationship can be roughly as valuable as a renewed one-year contract, because tenure and stickiness matter more than the paper. But she is firm that no contract at all drops a client into the break-fix bucket, worth roughly a tenth of a contracted client. Adam Borst is harder-line still: told a prospective seller had no contracts, just clients, his on-air response was that the value is zero, because without a signed relationship the clients are tied to the departing owner, not the business.

The takeaway is that diligence tests whether your revenue survives without you. Concentration and loose contracts both fail that test.

Owner dependence

Owner dependence is the lever owners control most and address least. If the business runs through your head and your relationships, a buyer discounts it, because the thing they are buying walks out the door with you. Daniel Welling of MSP Finance Team frames value as driven by two independent levers: scale, and owner detachment. Both move the multiple on their own. A business that still needs the founder in every important room is a riskier forecast, and it prices like one.

There is a sharper, financial version of this risk that surfaces in diligence as the quality-of-earnings review. Greg Bilzerian of NextGen Growth Partners describes the standard sequence: the seller claims 1M dollar EBITDA, the QoE review finds it is actually 600k dollar once owner comp and add-backs are honestly normalized, and on a 6x multiple that turns a 6M dollar deal into a 3.6M dollar deal. A lot of what reads as owner dependence is really owner economics never being separated from business economics. Reed Warren's practical test is the cleanest fix: mentally strip out owner perks and comp, replace yourself with a six-figure general manager, and see what EBITDA is left. That number, not the one that flatters your add-backs, is what a buyer underwrites.

The fix is not clever accounting. It is deputizing people so the business genuinely runs without you, well before a process starts. Do it early and it is cheap. Try to engineer it in the last year and buyers see the pattern in the financials and discount it anyway.

Growth rate and pricing power

Two MSPs with identical EBITDA are not worth the same if one is growing and one is flat. Buyers weight the historical growth trajectory as a proxy for forward growth, and Daniel Welling treats growth rate as a distinct lever from EBITDA size, one that moves the multiple independently. A durable double-digit grower reads as a compounding annuity. A flat book, even a profitable one, reads as a business the buyer has to work to grow, and they price accordingly.

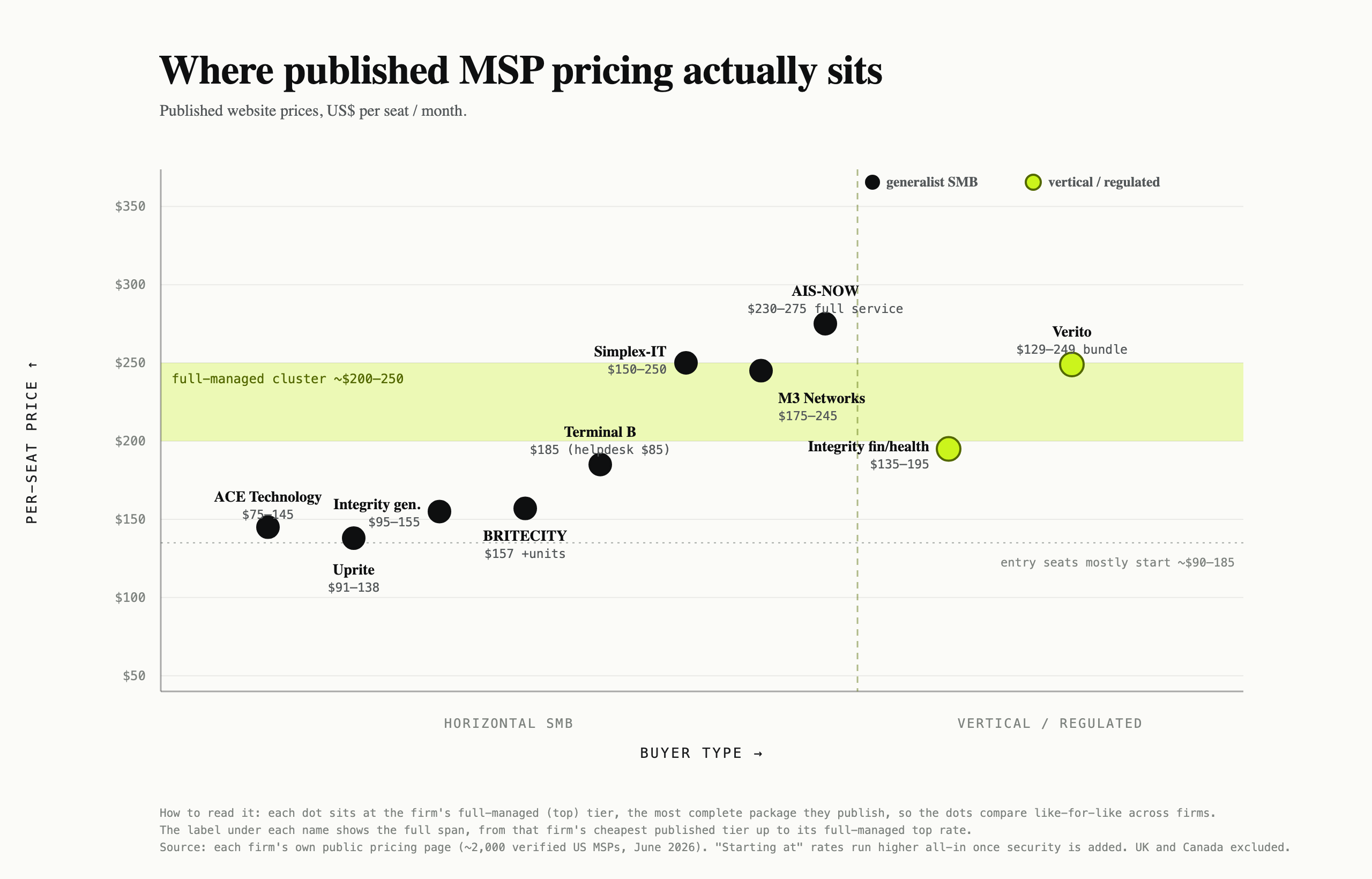

Pricing power is the quieter side of growth, and the one owners leave on the table most often. Our analysis of published MSP pricing shows how tightly the market clusters at the entry tier, which tells you two things: the floor is crowded, and the owners who have moved off it, through security, compliance, or vertical depth that justifies a higher per-seat price, are the ones with both better margins and the growth story buyers pay for.

Pricing power and the cyber scarcity lever are the same lever from two angles. Differentiation lets you charge more, and charging more shows up as both margin and growth, which is what re-rates the multiple.

The AI-spend trap

There is a wave of content telling MSP owners to AI-ify the business to boost the multiple. Be careful with it, because the mechanism runs the other way if you get it wrong. Buyers do not pay for AI spend. They pay for EBITDA. AI investment that destroys EBITDA destroys the price, and unproven automation spend is a liability at the table, not an asset.

The cautionary tale here comes from Abraham Garver, who advises MSP sell-side processes for a living. He describes a roughly 50M dollar-revenue MSP in the security and financial-services vertical that had been spending about 7m dollars a year on AI investment before ChatGPT, and had zero EBITDA left to show for it when the PE sponsor wanted to exit. His rule is exact: a patent, or an AI capability, is worth only what it demonstrably contributes to EBITDA. If it does not prove in the financials, it is not worth anything to a buyer.

This is not an argument against AI. It is an argument against confusing spend with value. Automation that lowers cost-per-endpoint and shows up as expanding margin is a real driver, the kind of operational proof buyers increasingly probe for in diligence. The test is the same one that governs every lever on this page: does it prove in the financials. If yes, it lifts the multiple. If no, it is a story, and buyers discount stories.

The insurance drift nobody prices

Here is a lever almost nobody covers, and it is worth knowing precisely because it is unglamorous and checkable. Doug Kreitzberg of SeedPod Cyber makes the observation: PE-backed MSPs are very good at buying companies and integrating services, and much less consistent at integrating insurance. After a tuck-in, the policy limits, deductibles, and exclusions lag the real size of the combined business. The company grows, the coverage does not keep up, and a gap opens between the risk the business now carries and the risk its policies actually cover.

Why does this matter for your multiple, on either side of a deal. If you are acquiring or rolling up, unpriced insurance drift is a liability you inherit, the kind careful diligence eventually surfaces and discounts. If you are the seller, clean, appropriately-sized coverage is a cheap signal that the business is genuinely buttoned up, the same category as documented runbooks and clean contracts. It will not win you a deal, but it can quietly cost you turns if a QoE process finds coverage that does not match the size of the book it is meant to protect. It fits the pattern of everything above: buyers pay for durability and discount hidden risk, and coverage that lags growth is exactly the kind of hidden risk that surfaces late.

What to build 2 years out, in priority order

If you want the platform band rather than the tuck-in band when a process starts, the work is not negotiation. It is groundwork, and it takes real time. Here is the priority order I would run, built from the levers above and weighted by how much they move the number against how long they take to fix.

- Get owner-independent. Deputize delivery first, then account management, then, hardest and last, new-business sales. This is the highest-leverage project and the slowest, which is why it goes first. A business that runs without you both clears diligence and reads as a platform rather than a job.

- Clean the recurring base. Move month-to-month clients onto real agreements, prune or reprice the break-fix stragglers, and get the recurring share comfortably above the line where the book reads as an annuity. Recurring revenue that is genuinely sticky is what a lender underwrites.

- Fix concentration and contracts. Diversify away from any single client near or above half your revenue, and get signed paper on the relationships that matter. Both directly remove discounts and reduce the odds you get pushed into an earn-out.

- Build the growth and pricing story. A durable growth trajectory and differentiation that supports higher pricing, whether that is real security depth or vertical focus, is what re-rates you inside your band. Commodity pricing caps the ceiling.

- Run the books like a seller. Monthly management accounts, honestly normalized EBITDA with owner economics stripped out, and coverage sized to the business. This is the cheapest item and it protects every one above it from being torn up in a QoE review.

Do this and you cross the thresholds that matter with a business that survives its own diligence. The full sequencing, month by month and against what diligence actually hits, lives in selling your MSP and exit readiness. The levers set the number. The two years before the process decide which levers you actually have.

FAQ

Size, because it is a threshold, not a slope. Crossing roughly 1M dollar EBITDA opens the private-equity buyer pool, and reaching about 3M dollar-plus EBITDA makes you a platform candidate rather than a tuck-in. Platform deals in our verified comp set priced at a 13.6x median against 7.8x for add-ons, so the jump from tuck-in to platform is the biggest single re-rating available.

Only if the capability is genuinely scarce. Scarce cyber deals like Thales-Tesserent at 24.1x and Datrix at 16.3x sit far above the 2 to 7x break-fix floor. But cross-selling a resold security product to your existing base is now table stakes, a one-time revenue bump, not a durable premium. A bolt-on SKU keeps you at the market 5 to 8x; a real MSSP practice a strategic cannot easily replicate is what earns the premium.

Only if it shows up in EBITDA. Buyers pay for profit, not for AI spend. One roughly 50M dollar-revenue MSP spent about 7m dollars a year on AI and had zero EBITDA to show for it at exit, which was worth nothing to a buyer. Automation that lowers cost and expands margin lifts the multiple. Automation that is a line item with no margin behind it is a liability at the table.

A lot, and it can change the deal structure entirely. High concentration pushes buyers toward earn-outs, so more of your money becomes contingent instead of guaranteed at close. In one advised deal, losing two or three clients worth about 200k dollars of recurring revenue between LOI and close triggered a 2M dollar valuation haircut. Diversifying away from any single client near half your revenue is one of the highest-return pre-sale fixes.

Two years at minimum, three is more realistic. The highest-leverage project, making the business run without you, is also the slowest, so it has to start first. Cleaning the recurring base, fixing concentration and contracts, and running monthly management accounts all take time to show a clean multi-year track record. Groundwork started early is cheap; the same fixes attempted in the last year read as engineering and get discounted in diligence.

Two newer lenses on the same question: the MSP Moat framework scores defensibility dimension by dimension, and cyber insurance requirements are quietly becoming a valuation floor of their own.

Getting exit-ready

If you own a business and expect to sell to private equity one day, the groundwork for a strong exit starts years before the process. I work with owners on exit readiness. Get in touch.