Four kinds of buyer purchase managed service providers, and each one prices your business on a different logic. Another local owner will pay 2 to 4 times EBITDA out of his own pocket. A strategic trade buyer or a private-equity consolidator folding you in as a tuck-in pays a median of 7.8 times. A PE fund buying you as its platform entry into the sector pays a median of 13.6 times. Search funds sit near the bottom at 3 to 5 times. The single most useful thing to understand before you talk to anyone is that the multiple you get is set less by how good your MSP is and more by which of those four seats the person across the table is sitting in.

I spent a decade in investment banking and private equity working on transactions north of $7bn, sat on the board through a $300m-plus PE exit, and now run growth inside MSPs and B2B service businesses. So I look at this from both sides: the deal seat that prices these companies, and the operating seat that lives inside one. This piece walks through who the four buyers are, what each pays and why, the one arbitrage that decides whether you capture a re-rating or get priced like a trade sale, and how to decide which buyer to court given your size and goals.

For what MSPs actually sell for across size bands, see MSP valuation multiples in 2026. For the method to run the number yourself, see how to value an MSP.

The four buyers, and what each one pays

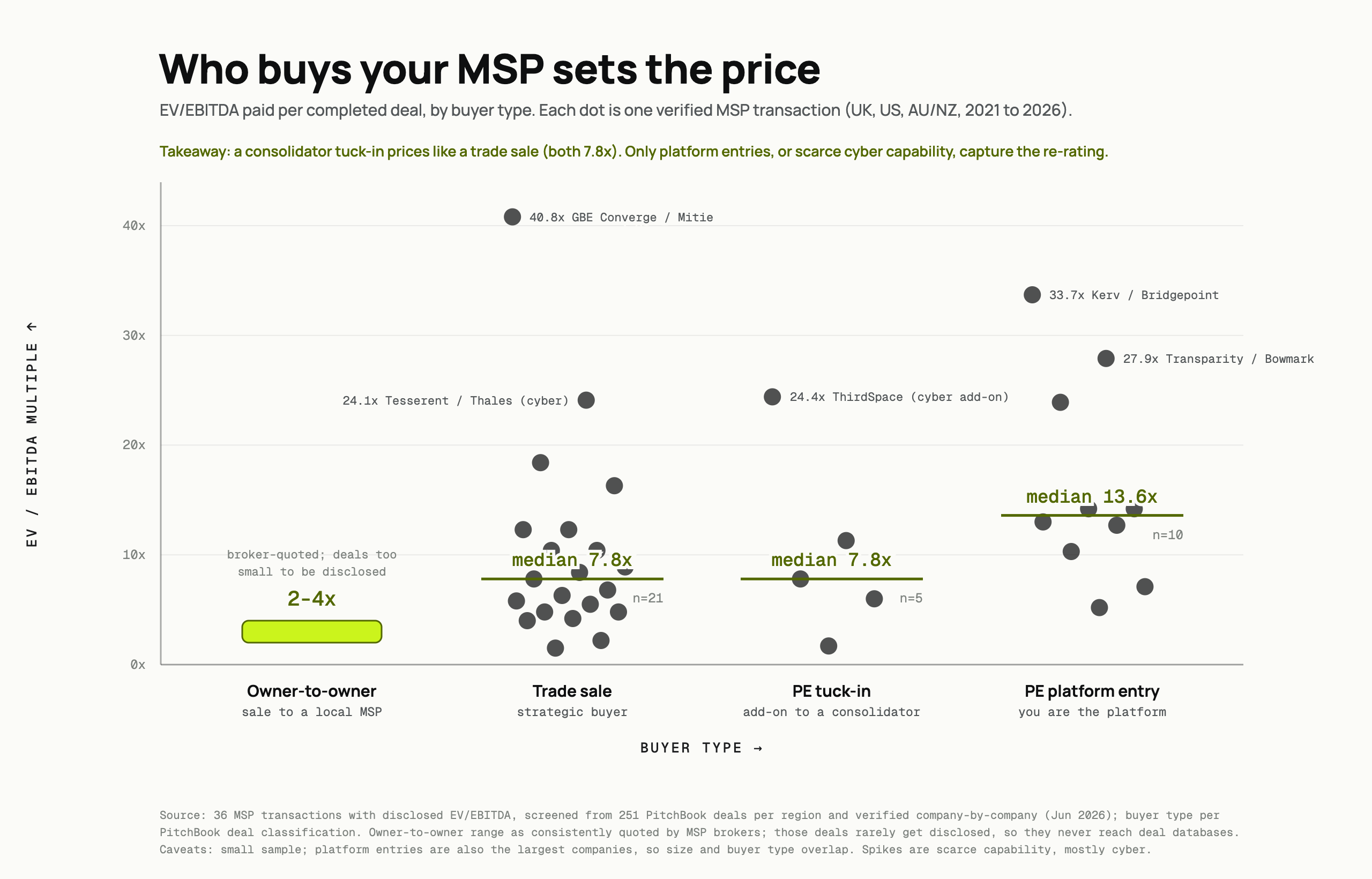

Start with the numbers, because the spread between them is the whole story. The table below comes from a verified comp set of 36 disclosed MSP transactions (US, UK and Oceania, 2021 onward) that I pulled from PitchBook and checked company by company. It splits the deals by who the buyer actually was.

| Buyer type | Median EV/EBITDA | What they are buying |

|---|---|---|

| PE platform / MBO | 13.6x | You, as the platform to build a sector roll-up on |

| PE add-on (tuck-in) | 7.8x | Bolt-on scale for a platform they already own |

| Strategic / trade | 7.8x | Your clients, capability or geography, folded into their business |

| Search fund | 3 to 5x | A cash-flowing business one operator can run and grow |

| Owner-to-owner | 2 to 4x | Your book of business, bought with personal or bank money |

Before you anchor on any of these, three honest caveats carried through from the underlying data. This is 36 disclosed deals, not a market census. The buyer types overlap with company size, because platform deals are the largest companies in the set, so the size ladder and the buyer type are partly confounded and 36 deals cannot fully separate them. The high spikes inside the strategic bucket are cyber-security scarcity, not typical trade pricing: Thales paying 24.1x for Tesserent, or Datrix at 16.3x, are sovereign-cyber and cloud-security assets, not ordinary MSPs. And the smallest end of the market, the owner-to-owner sales, never reaches a database like PitchBook at all, so it is invisible to every published median you will ever read.

Owner-to-owner: the invisible market where most MSPs actually trade

The buyer most likely to purchase a small MSP is another MSP owner down the road, and this is the part of the market nobody's data captures. These sales happen at 2 to 4 times EBITDA, paid from an owner's own savings or a bank loan, and they never surface in a transaction database because there is no listed acquirer to disclose them. On r/msp, one buyer laid out the ladder brokers had given him: 5x needs about $1M in revenue at a 22 to 25% margin, 6x needs roughly $1M of EBITDA, and 7 to 8x is rare and reserved for large regional players. His own standing offer for a 2-to-4-person shop was a flat 4x EBITDA, a short 3-to-6-month transition, no earn-out, and existing staff kept on.

Two things get priced in hard at this end. First, owner dependence. The community view is blunt: a solo operator's book is really just relationships with the owner, so it gets discounted to around 1x EBITDA or less unless the relationships are deliberately transferred. Second, the owner-salary add-back. Sellers routinely quote an EBITDA that assumes they take no salary, so an experienced buyer strips a market-rate manager's pay back out before trusting any multiple. One thread described a $350k-revenue shop advertising $200k of EBITDA that, once a real salary was subtracted, was closer to $25k, and worth maybe $75k rather than the $300k asked.

Strategic and trade buyers: they pay for scarcity, not scale

A strategic buyer is another operating company, often a larger MSP or IT services firm, buying you for your clients, a capability, or a geography they want. In the comp set these deals land at a 7.8x median, the same as PE tuck-ins. The floor is low, around 2 to 7x for VAR-style bolt-ons, which is why the strategic bucket's median EV/Revenue is only 0.72x. What lifts a strategic multiple is not size. It is scarcity. The two spikes in this bucket, Thales-Tesserent at 24.1x and Datrix at 16.3x, were both scarce cyber and cloud-security capabilities that a buyer decided were cheaper to acquire than to build.

You can hear the same logic from operators. One r/msp commenter described watching a very vertical, very sticky platform play sell at 100 times net profit, framing it as a one-off where the industry's "600-pound gorilla" found it cheaper to buy than build. Treat that number as folklore, not a comp. The point that survives is real: a strategic overpays only when you have something they cannot easily replicate, and for most MSPs that something is deep cyber or vertical depth, not another hundred generalist seats.

PE add-ons: a tuck-in prices like a trade sale

When a private-equity-backed consolidator buys you as an add-on to a platform it already owns, you are a tuck-in. The comp set puts these at a 7.8x median, identical to strategic sales. This is the finding most owners get wrong, so it is worth stating plainly. Being bought by private equity does not, by itself, get you a private-equity multiple. If you are the fourth or fourteenth acquisition bolted onto someone else's platform, you are priced like a trade sale, because functionally that is what you are: incremental scale for a machine that is already built.

PE platform entries: where the re-rating lives

The only PE deals that pay up are platform entries, where a fund buys you specifically to be the foundation of a sector roll-up. In the comp set these run to a 13.6x median. The reason is a genuine re-rating: the fund is buying a vehicle it will grow through leverage and add-ons, and it prices the whole thesis, not just your current EBITDA. The UK platform wave that disclosed its numbers shows the top of the range, with Kerv at 33.7x and Transparity at 27.9x as platform launches. But platform status has a floor. Investment banker Abraham Garver, who has advised on more than a dozen MSP platform deals, puts it around $3M of EBITDA on his podcast appearances: below that, the private-credit lenders who fund a leveraged buyout will not engage, so smaller targets get folded in as add-ons instead of becoming platforms themselves.

The insight: it is not that PE pays more, platforms get platform multiples

Line up the medians and the real mechanism is obvious. PE platform 13.6x, PE add-on 7.8x, strategic 7.8x. The headline "PE pays roughly 12x versus 8x for everyone else" is technically true and completely misleading, because it hides the fact that a PE tuck-in and a trade sale price identically. The variable that actually moves your number is not whether the acquirer is a private-equity firm. It is whether you are the platform or the add-on.

When PE buys you as the platform entry, you capture the re-rating: you are priced as the start of something. When a PE-backed consolidator tucks you in as an add-on, you get strategic-level pricing around 7 to 8x, and you are the one being arbitraged, because the buyer will fold your 8x EBITDA into a platform that the market values at 12x-plus. The premium exit, then, is to become a platform (or to be scarce, meaning real cyber or vertical depth) before the process starts. A consolidator tuck-in prices like a trade sale regardless of who ultimately owns the buyer. If you want to understand which levers push you toward platform pricing, that is the whole subject of MSP valuation drivers.

Search funds: the operator-buyer at 3 to 5x

A fifth buyer sits below all of this: the search fund. These are individual operators, often MBA-backed, who raise money to buy one business and run it themselves. Gui Carlos of N2M Capital puts search-fund pricing at 3 to 5x EBITDA in his 2026 MSP valuation guide, below PE tuck-ins and well below platforms. They are constrained by SBA-style financing and by the fact that a single operator, not a fund with a portfolio, is taking the risk. Search-fund buyer Greg Bilzerian, interviewed on the MSP Heroes podcast, described coaching owners with a $300k-EBITDA example trading at roughly 3 to 5x, or $0.9m to $1.5m, and pushing them to weigh who is buying and why rather than the top-line number alone.

For a sub-$1M-EBITDA owner, a search fund can be the most realistic institutional buyer available, and often a gentler one than a consolidator, because the operator intends to run the business rather than strip it. The trade-off is price. You are unlikely to see a platform multiple from someone buying a single business to operate personally.

The r/msp problem: operators hate PE and dream of selling to it

Spend an hour in the MSP community and the sentiment toward private equity is visceral. The most-upvoted framing on r/msp is that "private equity has ruined everything": PE-owned MSPs are described as places with no raises, no budget and brutal working conditions, and there are cautionary threads about PE buyers gutting acquired teams, cutting internal IT staff, and dropping or under-serving clients. Industry figure Karl Palachuk has argued the modern PE model is structurally broken because "the only thing that matters is a 20%-plus profit," achieved through layoffs and frozen product development. This is community sentiment, told as war stories rather than audited fact, but it is loud and consistent.

Here is the contradiction, and I think it deserves an honest hearing rather than a cheap dunk. The same owners who decry consolidation overwhelmingly plan to exit by selling, most likely to exactly the buyers they criticize. Benyamin Holley, a VC-backed founder in the space, named this directly on X: MSPs "decry" consolidation and post-acquisition product decay while their own personal dream is almost always to sell, and nobody in the industry resolves the tension. He is right that it goes unresolved, and I will not pretend to fully resolve it either.

From my seat, working inside a PE-adjacent MSP world, both halves are true at once and that is the uncomfortable part. PE genuinely does run some acquired businesses harder than the founder did, because a fund's job is to compress cost and grow EBITDA, and a founder's job was to keep clients and staff happy. And selling to a well-capitalized buyer is genuinely the cleanest liquidity event most owners will ever get, because a strategic or platform buyer can pay in a way a neighbor with a bank loan cannot. Hating the model and wanting its money are not hypocrisy. They are two accurate readings of the same buyer, one from the employee's chair and one from the owner's. The practical move is to price that duality into the deal terms, which is what the next section is about.

The roll-up story you have never actually read

Every roll-up account in circulation is told by a winner. Tim Conkle of The 20 MSP publicly states 44 acquisitions in three years, framed around alignment and a shared stack. A podcast clip on Evergreen claims 160-plus total acquisitions, 47 in 2025 alone, and $250m of portfolio EBITDA. Treat all of those as the operators' own claims, unverified against filings. Even when a roll-up admits an early mistake, it is delivered as a redemption arc, not a warning.

What is missing is the independent retrospective: a sourced, dispassionate account of what a named roll-up actually looked like 18 months after the deals closed, written by someone with no stake in the platform's story. It does not exist. Nobody has published the honest post-mortem, which means every owner deciding whether to sell into a roll-up is working from marketing on one side and forum anecdotes on the other, with nothing rigorous in between. That gap is worth naming out loud, because it changes how much weight you should put on any roll-up's own numbers. When the only detailed accounts come from the people selling the model, discount them accordingly.

There is also a fifth buyer emerging that almost nobody prices yet: insurance companies. Zurich agreed to buy Beazley with an MXDR arm attached, Coalition acquired an MDR shop outright, and Acrisure built a cyber services division from three MSP acquisitions. Their underwriting logic values a security book differently from any financial buyer. If your MSP carries real security revenue, read why insurers are buying MSSPs now before you pick a lane.

Which buyer should you court?

No competitor page turns "different buyers pay differently" into an actual decision. Here is the framework I would use, keyed to the two things that actually determine your options: your size and your scarcity. And whichever buyer you court, know what actually changes in the first 100 days after the wire hits before you sign anything.

- Sub-$1M EBITDA, generalist MSP. Your realistic buyers are another owner (2 to 4x), a search fund (3 to 5x), or a tuck-in into a nearby platform (up to ~7.8x if you have clean contracts and low owner dependence). You will not get a platform multiple. Court the tuck-in or the search fund, and spend the two years before a process reducing owner dependence, because that is what separates a 4x from a 7x at this size.

- $1M to $3M EBITDA, generalist. You are in the tuck-in and lower-mid strategic band, roughly 5 to 8x. Platform status is likely still out of reach because private-credit lenders want ~$3M-plus of EBITDA. Your job is to look like the best possible add-on: high recurring-revenue mix, multi-year or genuinely sticky contracts, no single client over 25% of revenue, and a management bench that runs without you.

- $3M-plus EBITDA, or scarce capability at any size. Now platform entry (13.6x territory) is genuinely on the table, and a scarce cyber or vertical asset can pull a strategic well above the 7.8x median (recall Tesserent at 24.1x). Court the PE platform buyers and the strategics who lack your capability, run a competitive process, and remember that being the platform, not the add-on, is where the re-rating lives.

Across all three, the buyer sets the ceiling and your readiness sets where in the band you land. The groundwork that moves you up the band, contract quality, client concentration, owner dependence and recurring-revenue mix, is exactly the diligence that a buyer will test, and it is covered in depth in selling your MSP and exit readiness.

No. Private equity only pays a premium when it buys you as a platform, at a median around 13.6 times EBITDA in our comp set. When a PE-backed consolidator tucks you in as an add-on, you are priced at a median of 7.8 times, the same as a strategic trade sale. The buyer being a PE firm does not by itself get you a PE multiple. Whether you are the platform or the add-on is what sets the price.

Search funds typically pay 3 to 5 times EBITDA, per the Gui Carlos / N2M Capital 2026 MSP valuation guide. They sit below PE tuck-ins and well below platform buyers because a single operator, backed by SBA-style financing, is taking the risk rather than a fund with a portfolio. For a sub-$1M-EBITDA owner, a search fund can still be the most realistic institutional buyer available, and often a gentler operator than a consolidator.

Most small MSPs are bought by another MSP owner in an owner-to-owner sale at 2 to 4 times EBITDA, paid from personal savings or a bank loan. These deals never appear in transaction databases because there is no listed acquirer to disclose them, so they are invisible to every published median. Buyers at this end discount heavily for owner dependence and strip out the owner-salary add-back before trusting any advertised EBITDA number.

Both readings are accurate from different chairs. From the employee's seat, PE can run an acquired MSP harder, cutting cost and raising margin targets, which is the source of the visceral community hostility on forums like r/msp. From the owner's seat, a well-capitalized buyer offers the cleanest liquidity event most founders will ever get, one a neighbor with a bank loan cannot match. Disliking the model and wanting its money are two true readings of the same buyer, not hypocrisy.

A strategic buyer overpays only for scarcity, not scale. In our comp set the strategic median is 7.8 times EBITDA, but the spikes are scarce cyber and cloud-security capabilities: Thales paid 24.1 times for Tesserent and Datrix went at 16.3 times. A strategic pays a premium when you have a capability it would rather buy than build, which for most MSPs means deep cyber or genuine vertical depth, not another block of generalist seats.

Getting to the right buyer

The buyer sets your ceiling, but your readiness decides where in the band you land, and that readiness is built years before anyone runs a quality-of-earnings review. If you own a business and expect to sell to private equity one day, the groundwork for a strong exit starts years before the process. I work with owners on exit readiness. Get in touch.