Cost-plus pricing sets your price from your inputs: a base labor rate multiplied by users, servers, and sites, with a margin bolted on top. It feels safe because it is arithmetic. The problem shows up years later, at the one moment the number really matters. When a buyer values your MSP, they do not pay for your cost stack. They pay for margin quality and pricing power, which are the two things a cost-plus mental model trains you to ignore. So the pricing method that feels the most disciplined is the one quietly holding your multiple at the floor.

I write this from the operator seat, not the broker seat. I spent a decade in investment banking and private equity working on over 7bn dollars of transactions, including a board seat through a 300m dollar-plus PE exit, and I now run growth inside a US MSP. So I have sat on both sides of this: the finance math that sets the multiple, and the day-to-day reality of pricing a managed-services book. The through-line of this piece is one I did not fully appreciate until I saw the two halves next to each other. How you price is a margin decision this quarter, and it is also a valuation decision that compounds all the way to your exit.

Every number here comes from our own verified pricing and transaction work, or from named, attributed practitioner sources. Where a figure is a practitioner's on-camera or public claim rather than confirmed deal data, I say so. For the underlying valuation comp set and the full source reconciliation, start with MSP valuation multiples in 2026. For the pricing models themselves, the companion piece is MSP pricing models in 2026.

What cost-plus pricing actually is

Strip away the labels and almost every MSP pricing tool in circulation does the same thing. It starts from a base hourly rate, estimates the effort to support a given environment, multiplies that by the count of users and servers and sites, and adds a margin. The pricing calculators that MSP peer communities hand their members are built exactly this way: one base rate, a stack of complexity multipliers, and a per-seat number that falls out the bottom. There is almost no reference in the math to what the service is worth to the client, or to what the market will bear. It is cost, plus a markup. Hence the name.

Here is the shape of it, with illustrative figures to make the mechanic visible. These are round numbers to show the logic, not a benchmark to copy.

| Input | Illustrative value | What it is |

|---|---|---|

| Base labor rate | 170 dollars per hour | Loaded cost of an engineer hour, the anchor for everything |

| Estimated effort per seat | 0.5 hours per user per month | A guess at how much support a seat consumes |

| Cost per seat | 85 dollars | Rate times effort, before any tools or margin |

| Tools and licensing per seat | 25 dollars | The stack you resell, roughly at cost |

| Target margin | 35 percent | The markup added on top of loaded cost |

| Resulting price | about 170 dollars per seat | What the client is quoted |

Nothing in that table is wrong as bookkeeping. You do need to know your loaded cost, and an MSP that cannot cover its cost stack does not survive to have an exit conversation. The trap is subtler. When the base rate is the only real input, the price becomes a function of your effort, not the client's outcome. Two clients who get the same peace of mind, the same uptime, the same board-level confidence pay the same 170 dollars whether that outcome is worth 200 dollars to them or 800 dollars. You have anchored your ceiling to your own labor cost. For the full per-seat build and the honest ranges behind it, see how much should an MSP charge.

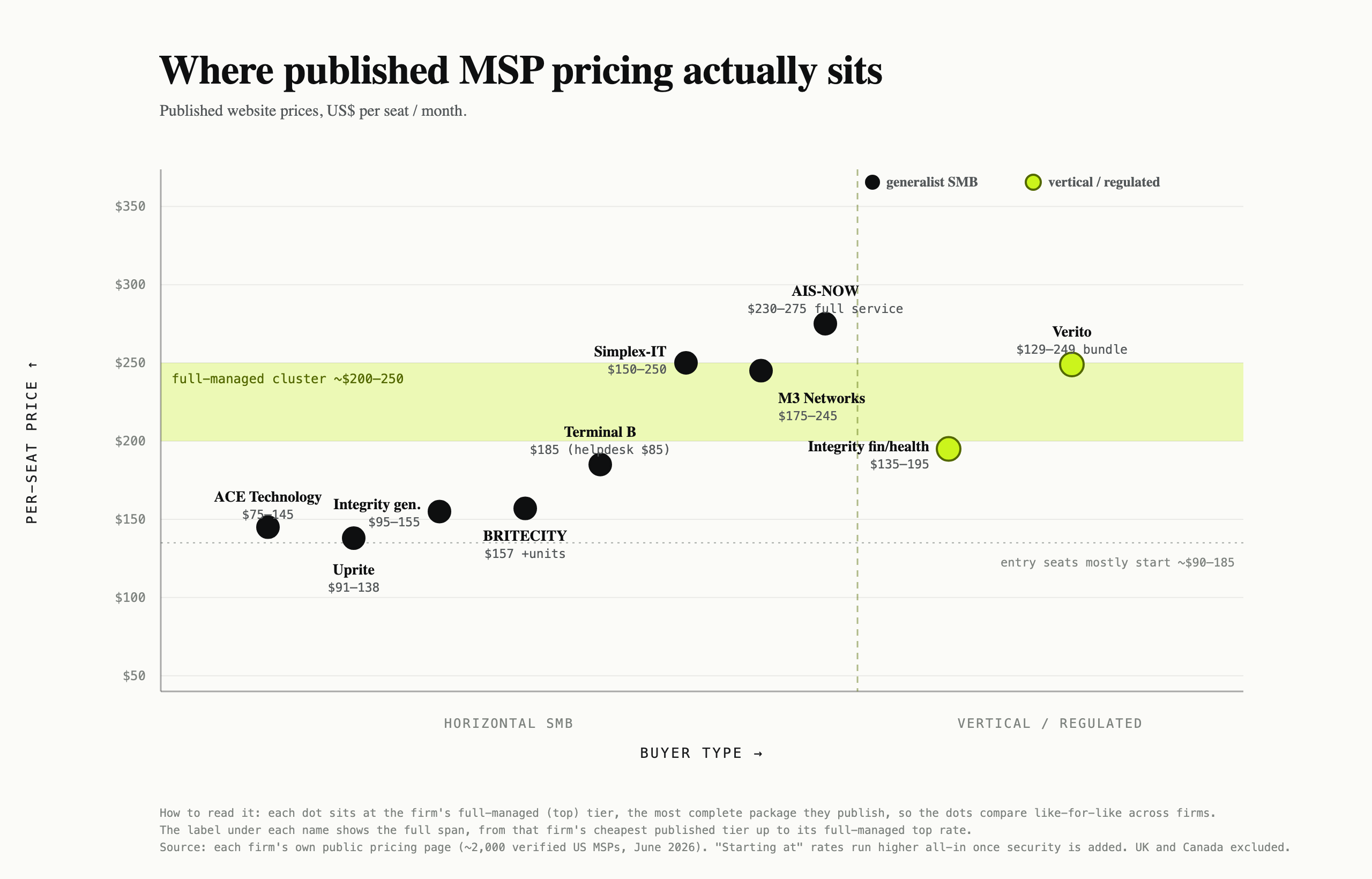

Where published prices actually sit

You can see the effect of this at market scale. When we scraped the public pricing pages of roughly 2,000 US MSPs in June 2026, the full-managed tier clustered tightly, most firms landing in a band around 200 to 250 dollars per seat, with entry tiers mostly starting in the 90 to 185 dollar range. The market is bunched, and it is bunched because most of it is priced the same way: off cost, off a base rate, off what the firm down the road charges.

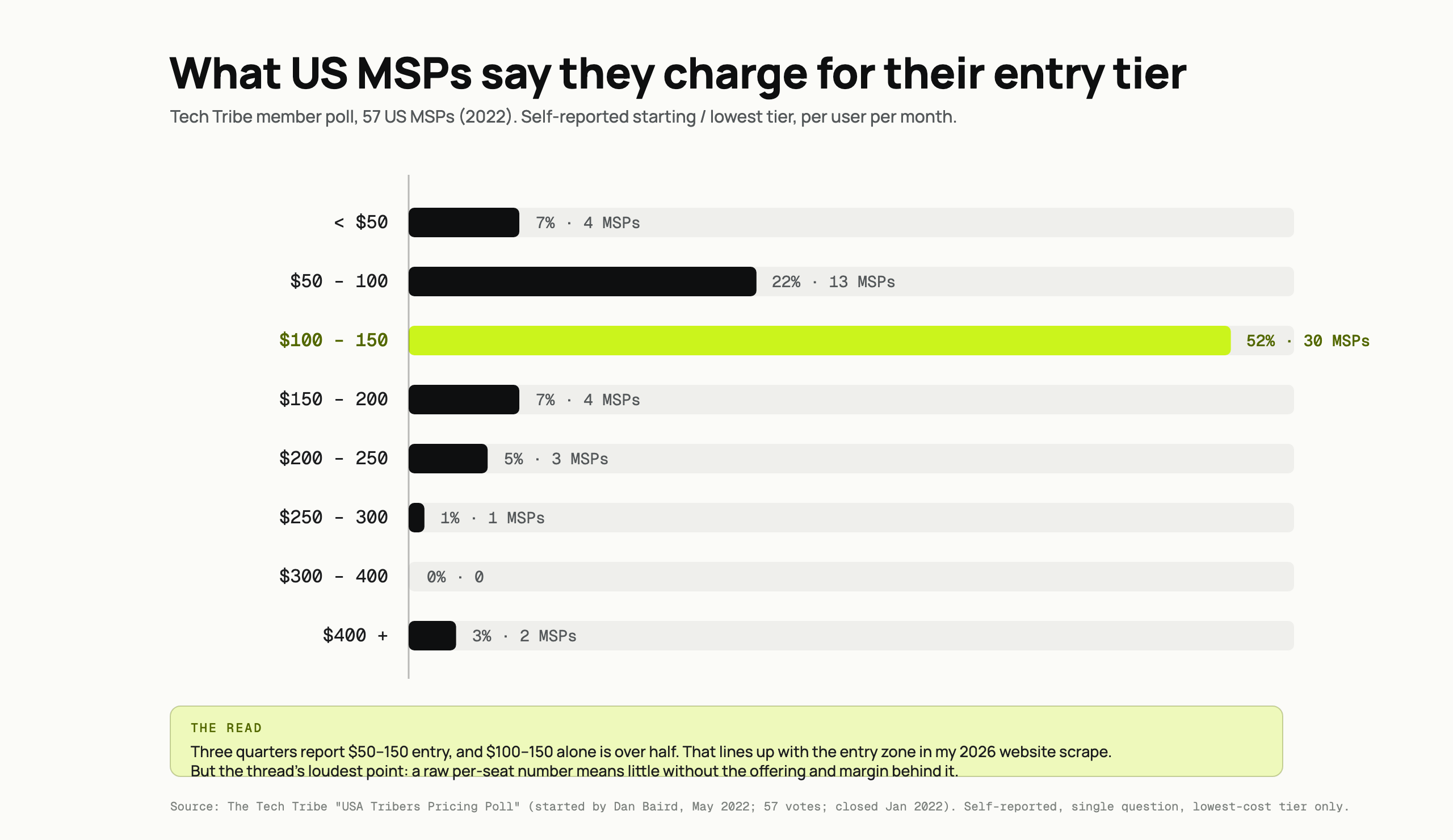

A 2022 community poll of 57 US MSPs points the same way at the entry tier. Over half reported an entry seat in the 100 to 150 dollar band, and roughly three quarters fell between 50 and 150 dollars. Cheap to run a poll, hard to argue with the shape: the entry floor is crowded, and everyone standing on it is standing there for the same reason. The loudest point in that thread was not a number at all. It was that a raw per-seat figure tells you almost nothing without the offering and the margin behind it, which is exactly the point a buyer makes years later at the valuation table.

The dots that sit above the cluster are the tell. They are the accounting and healthcare specialists, the firms that priced off a regulated vertical's need rather than off their own hourly rate. Same cost stack, roughly. Very different price, because they are selling a different thing.

Why buyers do not pay for your cost stack

Now move to the exit. A buyer valuing your MSP runs the business through a multiple applied to normalized EBITDA. They are underwriting the durability and quality of that profit, not the method you used to arrive at your prices. Two levers dominate what they pay: how much of your revenue is genuinely recurring and sticky, and how healthy and defensible your margins are. Cost-plus pricing is neutral-to-negative on both, and here is why.

First, the multiple itself is set by margin quality and size, not by top-line effort. Our verified comp set of 36 MSP transactions splits cleanly by buyer type, and the pattern is not about who pays more in the abstract. It is about what quality of business gets which multiple.

| Buyer | Median EV/EBITDA | What it means for you |

|---|---|---|

| PE platform / MBO | 13.6x | You are bought as the platform and capture the re-rating |

| PE add-on (tuck-in) | 7.8x | You are folded in and priced like a trade sale |

| Strategic / trade | 7.8x | Priced on scale and profit, with scarcity as the only exception |

The honest read on that table, straight from the data, is that it is not that private equity pays more. Platforms get platform multiples. And a tuck-in prices like a trade sale regardless of who ultimately owns the acquirer. The one thing that lifts a strategic buyer above the 7.8x line is scarcity, a genuine cybersecurity or vertical capability they cannot easily build, not a lower cost base. You do not get re-rated for running lean. You get re-rated for owning something the buyer pays a premium to acquire. Read the buyer split in full in what moves an MSP's multiple.

Second, the size ladder that decides which band you even qualify for is expressed in EBITDA, not revenue.

| Size band | Working multiple range |

|---|---|

| Owner-run, sub-1M dollar EBITDA | 3 to 6x |

| 1 to 5M dollar EBITDA, lower-mid | 5 to 10x |

| Platform, 5M dollar-plus EBITDA | 10 to 15x |

Notice what this does to a cost-plus operator. If your prices are pinned to your labor cost, then every efficiency gain you make, every automation that lowers your effort per seat, flows back to the client as a lower price rather than to you as margin, because your pricing formula recalculates off the lower cost. You work the effort down and hand the saving away. A value-priced peer holds the price, banks the automation as margin, and climbs the EBITDA ladder toward the next band. Same operational improvement, opposite valuation outcome. That is the quiet cap in action.

Pricing power is the lever cost-plus removes

Pricing power is the ability to hold or raise your price without losing the client, because the client is buying an outcome they value rather than an hourly rate they can shop. It is the single most valuable thing cost-plus pricing trains out of you, because a cost-plus quote invites the client to argue about your inputs. Charge off effort and every renewal becomes a negotiation about whether that server really takes that many hours. Charge off value and the conversation is about the outcome, where you have the stronger hand.

This shows up in diligence in a way that surprises owners. Buyers have started asking for operational proof that the business is getting more efficient over time, and they read that efficiency as a sign of a well-run, defensible book. Rhett Collver, an M&A voice in the channel, has argued publicly that buyers now want to see cost-per-endpoint trending down and resolution times dropping, and frames it bluntly as showing those numbers being how you move up the multiple ladder. The catch is that this only lifts your multiple if the efficiency shows up as your margin. Under cost-plus, it shows up as a lower price to the client and never reaches your EBITDA at all. Same operational win, and the value-priced operator captures it while the cost-plus operator gives it away.

There is a second-order version of this too. Pricing power is a proxy for the kind of business that does not depend on the owner. Shawn Freeman, who has written publicly about selling an MSP, makes the point that buyers pay more for a business that runs without you, one you could disappear from for 30 days and the work still gets done. A book priced on value, packaged into clear tiers a manager can sell and renew, is exactly that kind of business. A book priced on the owner's gut feel for what each client will tolerate walks out the door with the owner. The pricing method and the owner-dependence discount are the same problem wearing two hats.

Margin quality is the buyer's real scoreboard

If pricing power is the lever, margin quality is the gauge the buyer actually reads. And this is where cost-plus does its most insidious damage, because it produces margins that are both thinner and more erratic than they need to be, and a buyer's quality-of-earnings review is built to find exactly that.

Two things happen under cost-plus. The first is that margins drift down over time. When you never raise a price because the underlying cost has not changed, inflation quietly erodes the real margin every year, and the CPI escalator most agreements could carry goes unused because the price-increase conversation feels dangerous. The MSPs that never raise prices are not holding steady. They are discounting a little more each year and calling it stability. The second is dispersion. Client-by-client gross margin under cost-plus tends to swing widely, because the effort estimates that drive each price were guesses, and some clients turned out to consume far more support than the model assumed. A margin that ranges from the low 40s to the mid 70s across a handful of clients is not a sign of a healthy book. It is a sign that the pricing was never anchored to value, so some clients are subsidizing others.

A buyer's diligence flags both. Thin, drifting margin lowers the EBITDA the multiple is applied to. Volatile, dispersed margin reads as forecast risk and quality-of-earnings noise, which is exactly the kind of thing that turns a clean multiple into a discounted one. The buyer is not judging your pricing philosophy. They are judging the profit it produced, and cost-plus tends to produce profit that is lower and messier than the same book priced on value. For how a buyer actually normalizes and adjusts your earnings, see how to value an MSP.

The genuinely contested part

I want to be fair to the other side, because this is a real debate among good operators, not a settled question. The value-based pricing case is not free of problems. Value is harder to quantify than cost, so value-based tiers can feel arbitrary to a client and to a green salesperson. Cost-plus is teachable, defensible, and hard to get catastrophically wrong, which is precisely why the community's pricing tools default to it. A brand-new MSP that does not yet know its own cost stack has no business pricing on value it cannot yet articulate. There is a reason the base-rate calculator is the first tool a new owner reaches for, and it is not a bad first tool.

So the argument is not that cost-plus is stupid. It is that cost-plus is a floor you are supposed to grow off, and too many owners treat it as the permanent method. The tell is an owner who has run a profitable MSP for a decade and still prices every new client off the same base rate they used in year two, having never once tested what the market would actually pay for the outcome they deliver. That owner has a fine business and a capped multiple. The debate is real; the mistake is staying on the floor forever.

What I would do instead, in priority order

If the goal is a business that both runs well now and prices for a strong exit later, here is the order I would work the problem, weighted by how much each move lifts the multiple against how hard it is to do.

- Package before you price. Decide what goes in each tier and why before you put a number on it. A clear good-better-best structure, built around the outcomes clients actually value, is what lets you price on value instead of effort. Pricing is the last step, not the first.

- Move your best clients off cost-plus first. You do not have to reprice the whole book overnight. Take the clients who clearly get outsized value, a regulated vertical, a client whose downtime is catastrophically expensive, and price those on the outcome. That is where the pricing-power gap is widest and the risk of losing the client is lowest.

- Raise prices on a schedule, without apology. Use the CPI escalator your agreements can carry, and treat the annual increase as routine rather than a crisis. An MSP that never raises prices is discounting into a lower multiple one quiet year at a time. This is the cheapest margin lever you have and the one most owners refuse to pull.

- Track gross margin client by client. A simple monthly per-client margin tracker turns the invisible dispersion into a list of accounts to reprice or fire. Buyers reward a book with tight, healthy margins across clients, and you cannot fix dispersion you cannot see.

- Build one thing you are genuinely scarce at. Real security depth or true vertical focus is what earns pricing power and, at exit, the scarcity premium that lifts a strategic buyer above the trade-sale line. This is the slowest move and the highest ceiling, which is why it belongs on the list even though it takes years.

None of this is exotic. It is the difference between pricing your MSP like a job you do by the hour and pricing it like an asset someone will one day underwrite. The pricing method you choose today is compounding toward that valuation whether you are watching it or not. The full sequencing of what to fix in the two years before a sale lives in what moves an MSP's multiple, and the website-pricing decision that sits alongside all of this is covered in should an MSP put pricing on its website.

FAQ

Cost-plus pricing sets your price from your inputs: a base labor rate multiplied by the number of users, servers, and sites you support, plus the resold tool stack, with a target margin added on top. Almost every off-the-shelf MSP pricing calculator works this way. It is safe and teachable because it is arithmetic, but it anchors your price to your own effort rather than to what the service is worth to the client.

Buyers pay a multiple on your EBITDA, and they reward margin quality and pricing power, not a lean cost base. Under cost-plus, every efficiency gain flows back to the client as a lower price instead of to you as margin, so you never climb the EBITDA size ladder. The method also tends to produce thinner, more erratic margins, which a quality-of-earnings review flags as forecast risk and discounts.

No, and this is a real debate. Cost-plus is defensible, teachable, and hard to get catastrophically wrong, which is why it is the right first method for a new MSP that does not yet know its own cost stack. The mistake is treating it as permanent. It is a floor to grow off, not the method to price a mature, profitable book on a decade later, having never tested what the market would actually pay.

They do not judge your pricing method directly. They judge the profit it produced. A diligence process reads how much of your revenue is genuinely recurring and sticky, how healthy your margins are, and how consistent those margins are across clients. Cost-plus tends to produce lower and more dispersed margins than value-based pricing, so the same book prices worse. In our verified comp set, platform-quality businesses reached a 13.6x median against 7.8x for tuck-ins.

Start raising prices on a schedule. Most agreements can carry a CPI escalator, and the annual increase should be routine rather than a crisis conversation. An MSP that never raises prices is quietly discounting into a lower margin, and therefore a lower multiple, one year at a time. It is the cheapest lever available and the one owners most often refuse to pull.

Getting exit-ready

If you own a business and expect to sell to private equity one day, the groundwork for a strong exit starts years before the process, and how you price is part of it. I work with owners on exit readiness. Get in touch.